8 Easy Facts About Mortgage Investment Corporation Explained

8 Easy Facts About Mortgage Investment Corporation Explained

Blog Article

Mortgage Investment Corporation - An Overview

Table of ContentsWhat Does Mortgage Investment Corporation Mean?Not known Facts About Mortgage Investment CorporationThe Main Principles Of Mortgage Investment Corporation The Main Principles Of Mortgage Investment Corporation Indicators on Mortgage Investment Corporation You Should Know4 Easy Facts About Mortgage Investment Corporation Explained

After the loan provider sells the lending to a home loan capitalist, the lender can use the funds it obtains to make even more financings. Besides offering the funds for lending institutions to develop even more lendings, investors are necessary since they set guidelines that play a function in what kinds of loans you can get.As home owners settle their home mortgages, the settlements are gathered and distributed to the private investors who got the mortgage-backed safeties. Unlike federal government agencies, Fannie Mae and Freddie Mac don't guarantee loans. This means the exclusive financiers aren't guaranteed settlement if customers do not make their car loan payments. Given that the financiers aren't protected, adjusting financings have stricter guidelines for determining whether a debtor certifies or not.

Investors also manage them differently. Instead, they're sold straight from loan providers to exclusive investors, without involving a government-sponsored enterprise.

These companies will package the lendings and offer them to personal financiers on the second market. After you shut the financing, your lender might offer your lending to a capitalist, but this usually doesn't alter anything for you. You would still make settlements to the loan provider, or to the mortgage servicer that handles your mortgage payments.

Not known Details About Mortgage Investment Corporation

Just How MICs Source and Adjudicate Loans and What Occurs When There Is a Default Home loan Investment Corporations give capitalists with straight exposure to the genuine estate market with a pool of meticulously chosen home loans. A MIC is accountable for all aspects of the home mortgage spending procedure, from source to adjudication, including day-to-day administration.

CMI MIC Funds' strenuous credentials process allows us to handle mortgage high quality at the very beginning of the financial investment process, reducing the capacity for repayment concerns within the loan profile over the term of each home loan. Still, returned and late payments can not be proactively managed 100 per cent of the moment.

We purchase home loan markets across the country, allowing us to provide anywhere in Canada. To read more regarding our investment process, call us today. Get in touch with us by completing the kind below for even more information about our MIC funds.

The 6-Minute Rule for Mortgage Investment Corporation

At Amur Capital, we aim to supply an absolutely diversified method to alternate investments that make the most of home yield and funding conservation. By using a variety of traditional, revenue, and high-yield funds, we provide to a series of investing purposes and preferences that suit the needs of every individual investor. By buying and holding shares in the MIC, investors obtain a symmetrical possession passion in the firm and receive revenue via reward payments.

Furthermore, 100% of the financier's resources obtains positioned in the picked MIC without ahead of time deal charges or trailer charges - Mortgage Investment Corporation. Amur Resources is concentrated on supplying financiers at any kind of level with access to expertly handled personal mutual fund. Investment in our fund offerings is readily available to Alberta, British Columbia, Manitoba, Nova Scotia, and Saskatchewan homeowners and need to be made on a private placement basis

Purchasing MICs is a fantastic way to get exposure to Canada's growing property market without the demands of active building administration. Other than this, there are a number of other reasons why financiers consider MICs in my site Canada: For those seeking returns similar to the securities market without the linked volatility, MICs offer a secured actual estate financial investment that's simpler and might be a lot more lucrative.

Actually, our MIC funds have actually historically supplied 6%-14% annual returns. * MIC financiers receive rewards from the rate of interest settlements made by customers to the home mortgage lender, creating a consistent passive revenue stream at higher rates than typical fixed-income safety and securities like federal government bonds and GICs. They can also choose to reinvest the dividends right into the fund for compounded returns.

Mortgage Investment Corporation Fundamentals Explained

MICs currently represent approximately 1% of the total Canadian mortgage market and represent an expanding sector of non-bank economic firms. As capitalist need for MICs grows, it is necessary to comprehend exactly how they function and what makes them various from conventional property financial investments. MICs buy mortgages, unreal estate, and consequently give exposure to the real estate market without the included danger of property ownership or title transfer.

usually between six and 24 months) (Mortgage Investment Corporation). In return, the MIC collects rate of interest and charges from the customers, which are after that dispersed to the fund's favored investors as dividend payments, normally on a regular monthly basis. Due to the fact that MICs are not bound by several of the exact same strict loaning requirements as conventional financial institutions, they can establish their own requirements for accepting financings

Home mortgage Investment Corporations also appreciate unique tax treatment under the Earnings Tax Act as a "flow-through" investment vehicle. To stay clear of paying revenue tax obligations, a MIC needs to disperse 100% of its web earnings to investors.

Things about Mortgage Investment Corporation

In the years where bond returns continually decreased, Home mortgage Investment Companies and other different assets grew in appeal. Returns have recoiled given that 2021 as reserve banks have actually elevated rates of interest but real returns stay adverse relative to rising cost of living. Comparative, the CMI MIC Balanced Home mortgage Fund produced an internet yearly return of 8.57% in 2022, not unlike its efficiency in 2021 (8.39%) and 2020 (8.43%).

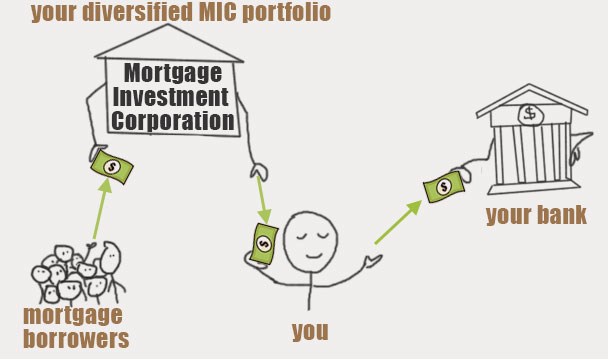

MICs provide investors with a means to invest in the genuine estate market without really owning physical residential or commercial property. Instead, financiers merge their money with each other, and the MIC uses that cash to money home loans for debtors.

The Main Principles Of Mortgage Investment Corporation

That is why we wish news to assist you make an informed decision concerning whether or not. There are many advantages associated with buying MICs, consisting of: Since financiers' cash is pooled with each other and spent throughout multiple residential or commercial properties, their profiles are expanded throughout various realty types and debtors. By owning a profile of home mortgages, financiers can reduce threat and stay clear of placing all their eggs in one basket.

Report this page